Does Ruger have real problems?

The saga continues

Ruger reported quarterly results three days ago. Beretta had a lot to say about it!

“The Company’s fourth quarter and full-year 2025 results underscore a clear and growing disconnect between management’s rhetoric and actual performance – a disconnect that cannot be explained away as cyclical or temporary headwinds. Instead, these results appear to reveal a management team and Board that are failing to execute effectively and are doubling down on a failed strategy that is eroding value for shareholders, employees and customers.

Based on Beretta Holding’s centuries of operating experience in the global firearms industry, including significant manufacturing and commercial operations in the United States, we review these results with a practical understanding of what disciplined execution and profitable growth should look like. Through that lens, the trajectory reflected in Ruger’s recent performance is deeply concerning.

Ruger reported what superficially looks like modest top-line growth – 3.6% for the fourth quarter and less than 2% for the full year – yet this figure masks the reality that revenue growth lagged inflation and came at the expense of profitability. Gross profit declined by 18.7% for the fourth quarter and by 29% for the full year, indicating that the Company’s strategy relies on buying sales at the expense of margin expansion and shareholder value. Management and the Board have so little real ‘skin in the game’ that they simply do not bear the brunt of their underperformance in the same manner that Ruger shareholders do.

This margin erosion is particularly troubling given management’s repeated emphasis on new products, which now represent more than 30% of sales and are purportedly central to Ruger’s growth strategy. Innovation should strengthen pricing power and support margin expansion. Instead, average selling prices declined to $364 in 2025 from $377 in 2024, further compressing margins and raising serious questions about the viability of the Company’s product strategy.

Earnings performance compounds these concerns. Adjusted EPS missed consensus, and on a GAAP basis, the Company swung to a loss for the year. Operating income deteriorated by nearly $65 million over the last two years, falling from $52 million in 2023 to an operating loss of $12 million in 2025. Over the same period, general and administrative expenses increased by over 25% from $42.7 million to $54.2 million. The Company’s inefficient and suboptimal capital allocation strategy remains a concern. In our view, Ruger’s decision to pay dividends in a year of negative earnings represents an unsustainable attempt to appease shareholders when that capital would be better deployed to support long-term earnings growth.

This is not the pattern of a company executing with discipline – it is the pattern of a business sacrificing financial health for the illusion of momentum. Further, the Board’s defensive posture toward its largest shareholder and refusal to engage meaningfully on strategy only amplifies concerns about governance. Assertions that recent board refreshment equips Ruger to oversee the ‘Ruger 2030’ strategy ring hollow when the strategy’s key elements are producing deteriorating margins, lost earnings power and negative real growth.

Ruger employees, customers and shareholders deserve better accountability and a strategic reset that prioritizes operational excellence and real value creation. The Company’s financial performance underscores that meaningful change is required to restore profitability and rebuild trust with employees, customers and shareholders. Beretta Holding’s nominees bring the governance experience, capital allocation discipline and industry expertise that we believe is necessary to strengthen oversight in the boardroom and help put Ruger back on a path toward sustainable shareholder value.”

Ruger’s stock hasn’t reacted much in the light of Beretta’s potshot. Which makes sense, the quarter was “meh”. Despite the mentions of average selling price and margin deterioration, the entire industry had a bad Q4, so something like this performance would make sense. NSSF estimated industry unit volume down -3.7% in the quarter:

The narrative for the quarter is overall volumes down, and Ruger taking share with their lower priced-SKUs. Which is a niche! Folks are trading down for lower ASP guns, consistent with Ruger’s sales quarterly growth and lower ASP. But of course, truth can be the first casualty in a proxy war.

Beretta’s claims here are not even wrong: yes, margin deterioration occurred. Yes, lower ASPs were to blame. But no, industry headwinds can be blamed here. They’re definitionally gaining share in the market as it trades down. Only around 20%~ of Ruger’s products could be considered premium, so this is to be expected in a bad quarter.

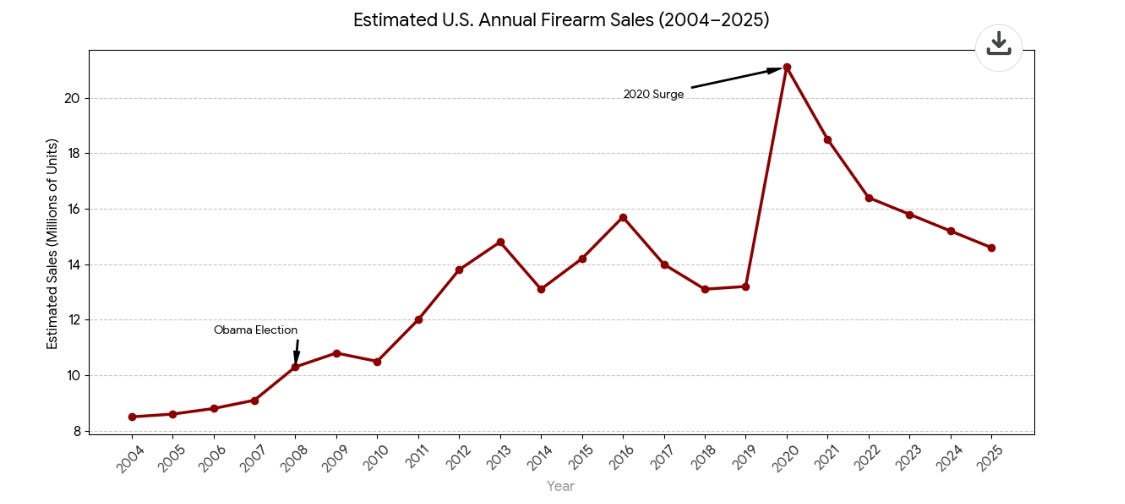

It’s the same story for all of FY25, but Beretta’s in the middle of a PR campaign. Part of why Beretta’s getting involved now is because of the overall macro and cyclical environment. We’ve seen 5 straight years of declines in sales since the COVID spike.

Gun buyers tend to stock up along large geopolitical regime changes. Beretta’s rationale is that an anti-gun regime will take over, either this year in the midterms or in 2028. The cycles are real and Beretta are doing their best to time the market.

This loops around to the idea of '“trough earnings”. Ruger trades for 10x forward EV/EBITDA. In cyclical industries, trough earnings refers to the lowest point of a given company’s profitability during an industry-wide downturn. Because fixed costs (like firearm factories and specialized labor) remain high even when demand drops, operating leverage cuts earnings at low volumes to make the business look worse than an “average” year. The goal is often to buy when multiples look high—meaning earnings have bottomed out but the market is starting to anticipate the recovery. In the 2024–2025 cycle, Ruger hit their trough as inventory gluts and political relief combined to crush margins.

Premiumization (or selling higher priced SKUs) acts as a survival mechanism during these troughs by shifting the focus from volume to ASP. This is what mix shift is— and why I called the quarter “meh”. Ideally, when Ruger unit volume drops, the company can defend its bottom line by selling higher-margin, SKUs that aren’t affected by economic swings. Beretta is correct to point this out in their press release; Beretta’s product portfolio is much more skewed toward premium that Ruger.

Counterintuitively, premium options often do best during the down-cycle in terms of relative performance. While an up-cycle lifts all boats, a down-cycle acts as a filter. In an up-cycle, budget products explode in volume because everyone has discretionary cash; however, in a down-cycle, the budget buyer disappears first, while the collector or professional continues to buy premium gear. Consequently, a portfolio that is 25% premium (like Ruger’s Marlin and Custom Shop lines) is supposed to provide a margin cushion that prevents trough earnings from turning into a disaster. But it didn’t happen in 2025— that’s where Beretta sees the opportunity. Beretta’s buying at a reasonable multiple even if earnings drop further— although the real upside is that we’re already at the bottom.

Previous coverage of the Beretta/Ruger proxy fight can be found here, with more posts in the archive. It’s all free: