Breaking down the Sonida for CNL Healthcare deal

Pop your collar

Sonida Senior Living (SNDA) continues to execute their senior living facility roll-up strategy with the acquisition of CNL Healthcare Properties (formerly CHTH), closing today. Coincidentally, SNDA announced earnings today with progress in RevPAR, NOI margin, and occupancy. Of course, occupancy is the straw that stirs the drink. The stock is trading down, but we’re most interested in the structure here because it is quite interesting.

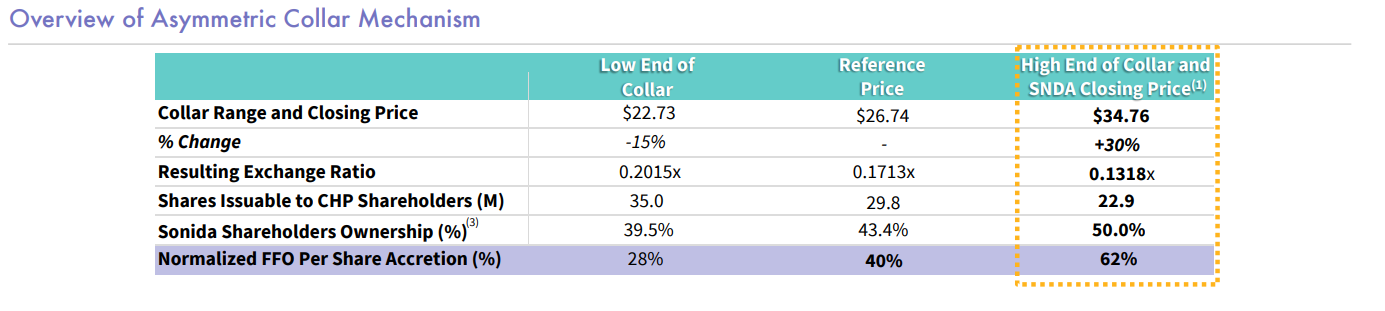

CNL was a thinly traded OTC business. Sonida, to protect both parties from stock volatility between the deal’s announcement and today’s close, the merger utilized an asymmetric collar on the exchange ratio (the stock-for-stock portion of the deal).

The total consideration for CNL shareholders was fixed at $6.90 per share, but the “ingredients” of that price were split. Every CHP share received $2.32 in cash and $4.58 worth of SNDA stock. Because the value of SNDA stock fluctuates daily, the collar was used to determine exactly how many SNDA shares it takes to equal that $4.58.

The collar acts as a safety net. It ensures that if SNDA’s stock price drops, CHP shareholders get more shares to keep their value at $4.58. Conversely, if SNDA’s stock price skyrockets, Sonida doesn’t have to give away too much of the company; they issue fewer shares, capping the dilution.

Floor- $22.73: If the SNDA 10-day VWAP stays below this price, the exchange ratio is fixed at its maximum. More share to CHTH.

Ceiling- $34.76: If the SNDA 10-day VWAP rises above this price, the exchange ratio is fixed at its minimum. Less shares to CHTH

The Floating Range: Between these two prices, the exchange ratio adjusts dynamically to maintain the $4.58 value.

The number of shares issued per CHP share is calculated by the $4.58 reference value divided by the 10-day VWAP during the 10-day measurement period prior to today’s close.

Sonida wouldn’t issue more than .2015 shares per CHTH share, nor would it issue less than .1318 per share. All that had to happen was that SNDA had to trade at 34.76 in the 10-day leadup to the deal close. And they hit the target! Sonida management was highly confident in the accretion story and wanted to ensure they didn’t over-dilute existing shareholders if the market rallied behind the news. They called it correctly!

It should be noted, fewer shares means higher steady-state FFO. Here’s a great slide from today’s IR release:

Love to see financial engineering work out!

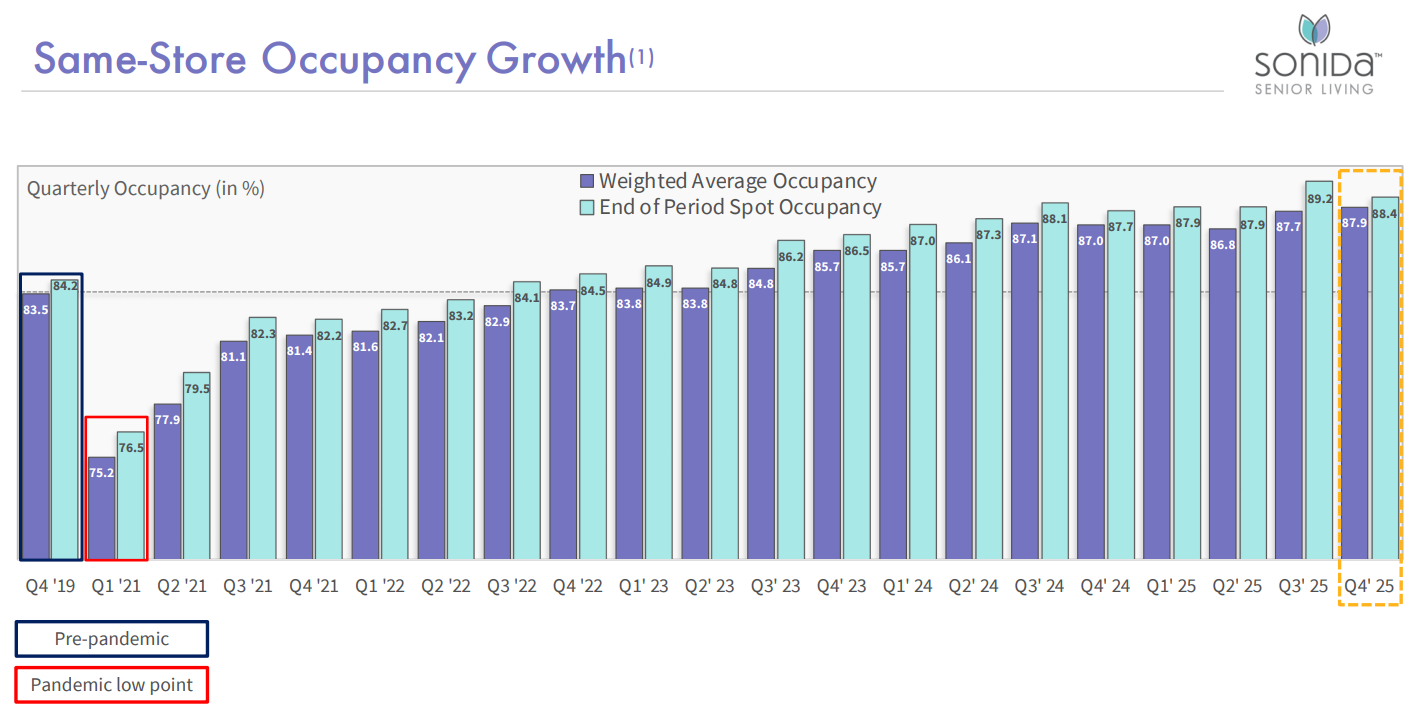

Regarding occupancy, Sonida’s strategy is to roll-up undermanaged assets. This means they want to either push price or push occupancy— whichever the asset needs to capture operating leverage. So when large deals close, we might see either RevPAR or occupancy drop as the new assets dilute the total spot occupancy of the portfolio:

A fantastic hotelier once told me that if you’re ever at full occupancy, you’re charging way too little. And that 95% occupancy is the sweet spot. Metrics keep marching forward— this is probably the #1 demographic secular growth story we’ll see in our lifetimes. There’s a number of public companies here with operating scale (Ventas, Welltower, SNDA, Brookdale). The whole basket will do well if the world keeps spinning for the next 20 years (big if!).

Thanks for sharing. Really interesting theme. Have you looked at NHI ?